In a world of rapidly changing customer experiences as well as the content consumption habits of the audiences, a full service video streaming platform provider was looking for ensure the best connectivity, quality and user experience for its product platform to maintain its competitive edge.

Incedo brought its considerable expertise in data science, analytics, cloud and design to create a specialised media lab as an incubation centre to support development, enhancement and re-engineering of the various product applications including the development of content sharing apps for mobile and OTT devices. The efforts resulted in the following:

Increased scalability, achieved reduction in functional time ensuring Reduction in go-to-market time and operations cost by 50%

Zero downtime through proactive service monitoring, reduced consumer complaints and increased download rates for the apps, maximized revenue from day one with reduction in OTT platform build release time from 12 hrs to 1 hr.

Enhanced viewer experience with smoother streaming and progressive downloads, through adaptive protocols for high-quality streaming (HLS, RTMP, MPEG-DASH).

Successfully initiated an app for Apple TV through the incubation centre.

Improved and extended Device compatibility leading to increased New Client Wins.

A US-based mortgage solution provider and a full-service lender servicing customers for more than three decades wanted a scalable solution that optimizes agility with minimal costs. They wanted a self-serving loan solution based on the changing load requirements of concurrent users.

So when our client wanted a self-serving loan solution for its end customers, while reducing customer service overheads, Incedo rose to challenge to help them build a platform that reduces the frequent downtime, eliminating the capacity and load related issues, while radically reducing the processing time.

With new solutions and a platform in place, the client generated results through:

Cost saving of $1 million, spread over a three-year period, in license fees.

Agility to scale and seamlessly manage and optimize underutilized services as well as demand spikes, reducing infrastructure costs with timely reviews and reporting

Self-serving portal for customers to have a better control over their account thereby reducing manual intervention of customer care team and reduced process time, leading to an improvement in customer acquisition, retention, and lower customer service overheads.

Intuitive and superior UX for a superior customer experience.

100% availability of loan portal, high performance with low latency and response time.

Our client, one of the leading biotechnology company had a Commercial Copay Program. These Copay Programs are designed to address patient financial barriers to treatment, promote patient adherence to therapy and enable prescribers to provide the most appropriate treatment option without patient financial concerns. So when the client was looking to improve adoption and utilization for its Commercial Copay Program, Incedo helped gain insights on strategic account planning as well as provide solutions regarding the program enrollment and copay utilization.

Incedo’s solution significantly reformed the efficiency of identifying and matching prescribers based on the prescriber’s demographics using fuzzy logic. This mapping was used to report accurate copay enrolments and claims metrics. Upon analyzing and understanding the business metrics and refining them properly to report relevant information, the solution resulted in the following:

Empowered field reps in new expanded roles with adoption and utilization insights through business intelligence reports to significantly increase customer acquisition. Field reps were enabled to provide proactive support to prescribers by identifying areas of low co-pay program enrollment and/or utilization.

Copay optimization for each brand and geography leading to optimized costs with optimal coverage amount for each brand/insurance plan.

Increased customer engagement with better collaboration and coordination across a territory board, by identifying opportunities where copay program utilization occurs for a product but not for other products.

By introducing fuzzy logic, the IDs for 26% (9,519) additional records were mapped as compared to the traditional logic

Manual intervention reduced due to fully automated python fuzzy match system

COVID-19 pandemic has brought a significant change in the way financial advisors manage their practices, clients and home office communication. Along with the data driven client servicing platforms, smooth transition and good compensation, advisors are closely evaluating their firm’s digital quotient to provide them the service and support in times of such crisis and if not satisfied, may look out options of switching affiliation during or post this crisis.

This pandemic is not a trigger rather has provided additional reasons for advisors to continue to look out for a firm that fits better in their pursuit of growth and better client service.

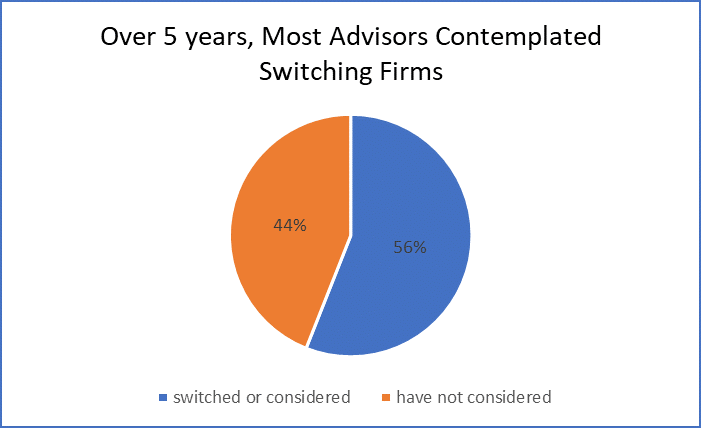

2018 Fidelity Advisor Movement Study says, 56% of advisors have either switched or considered switching from their existing firms over the last 5 years. financial-planning.com publishes that one fifth of the advisors are at the age of 65 or above and in total around 40% of the advisor may retire over the next decade.

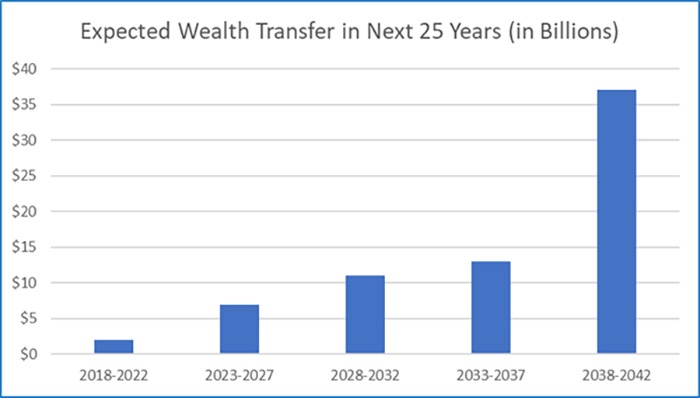

A Cerulli report anticipates transition of almost $70 trillion from baby boomers to Gen X, Gen Y and charity, over the next 25 years. Soon, the reduction in the advisor workforce will create a big advice gap, that the wealth management firms will have to bridge by acquiring and retaining the right set of Advisors

We are observing a changing landscape of advisor and client population, mounting cost pressure due to zero commission fee and the need for scalable operations. COVID-19 has further accentuated the need for the firms to better understand the causal factors for changes in advisor affiliation, to optimize their resources deployed for engaging through the Advisor life cycle. The wealth management firms are increasingly realising thata one fit for all solution may not get optimal returns for them.

Data and Analytics can helpthe firms segment their advisors better and drive better results throughout the advisor life cycle. Advisor Personalization, using specific data attributes can deliver contextual and targeted engagements and can significantly improve results by dynamically curating contextual & personalized experiences through the advisor life cycle.

A good data driven advisor engagement framework defines and measures key KPIs for each stage of the advisor lifecycle and not only provides insights on key business metrics but also addresses the So What question about those insights. As wealth management firms collect and aggregate data from multiple sources, they are also increasingly using AI/ML based models to further refine advisor servicing.

Let us look at the key goals or business metrics for each stage of the advisor life cycle below and see how data and analytics driven approach helps in each stage of the life cycle.

Prospecting & Acquisition

To attract and convert more high producing advisors, recruitment teams should be tracking key parameters through the prospecting journey of the advisors so that they can identify:

What is the source of most of their prospective advisors; RIA, wirehouses, other BDs

Which competitors are consistently attracting high producing advisor

What % of advisors drop from one funnel stage to another and finally affiliate with the firm

What are the common patterns and characteristics in the recruited advisors

Data driven advisor recruitment process that relies on the feedback loop helps in the early identification of potential converts, thereby balancing the effort spent on recruited vs lost advisors. It also improves the amount and quality of the recruited assets.

For example, analysis of one-year recruitment data of a large wealth management firm revealed that prospects dealing with variable insurance did not eventually join the firm due to the firm’s restricted approved product list. Another insight revealed that prospects with a higher proportion of fee revenue vs the brokerage revenue increased their GDC and AUM at a much faster rate after one year of affiliation. Our Machine Learning Lead Scoring Model used multiple such parameters and scored a recruit’s joining probability and 1-year relationship value to help the firm in precision targeting of high value advisors. These insights allowed the firm to narrow down their target segment of advisors and improved conversion of high value advisors.

Growth & Expansion

A lot of focus during the growth phase of the advisor lifecycle is on tracking business metrics such as TTM GDC, AUM growth, commissions vs Fee splits. The above metrics however have now become table stakes and the advisors expect their firms to provide more meaningful insights and recommendations to improve their practices. Some of the ways, firms are using data to enhance advisor practice are by:

Using data from data aggregators and providing insights on advisor’s wallet share and potential investment opportunities

Providing peer performance comparisons to the advisors

Providing next best action recommendations based on the advisor and client activities

For example, our Recommendation Engine analysed advisor portfolio and trading patterns and determined that most of the high performing advisors showed similar patterns in Investment distribution, asset concentration, churning %. This enabled the engine to provide targeted investment recommendations for the other advisors based on their current investment basket and client risk profile. The wealth management firms are also using advisor segmentation and personalization models based on their clients, Investment patterns, performance, digital engagement, content preference and sending personalized marketing and research content for the advisors based on their personas thus driving better engagement.

Maturity and Retention

It is always more difficult and costly to acquire new advisors as compared to growing with the existing advisor base. The firms pay extra attention to ensure that their top producer’s needs are always met. Yet despite their best efforts, large offices leave their current firms for greener pastures or higher pay-outs. The firms run periodic NPS surveys with their advisor population which indicates overall satisfaction levels of the advisors, but they do not generate any insights for proactive attrition prevention. Data and analytics can help you identify patterns to predict advisor disengagement and do targeted proactive interventions.

For example,our attrition analysis study for a leading wealth manager indicated that a large portion of advisors over the age of 60 were leaving the firm and selling out their business. This enabled the firm to proactively target succession planning programs at this age demographic of advisors. Our analysis also indicated a clear pattern of decreased engagement with the firm’s digital properties and decreasing mail open rate, for the advisors leaving the firm. Based on factors such as age, length of association with the firm, digital engagement trends, outlier detection, our ML based Attrition Propensity model created attrition risk scores for advisors and enabled retention teams to proactively engage more with at-risk advisors and improve retention.

As per a study from JD Power, wealth management firms have been making huge investments in new advisor workstation technologies designed to aggregate market data, client information, account servicing tools and AI-powered analytics into a single interface. While the firms are investing heavily in technology, only 48% advisors find the technology their firm is currently using, to be valuable. While only 9% of advisors are using AI tools, the advisor satisfaction is 95 points higher on a 1000-point scale when they use AI tools. Advisors find a disconnect between the technology and the value derived from the technology.

This further necessitates the need for personalised solutions for advisors and an AI driven Advisor personalisation platform which provides curated insights to the firms. This helps in targeted & personalized services & support to advisors through the Advisor lifecycle, enabling optimal utilization of the firm’s resources and unlocking huge growth potential.

The firms that will understand the potential of data driven decision making for their advisor engagement and will start early adoption of such tools will thrive in these uncertain times and will emerge as a winner once the dust settles.

COVID-19 pandemic brought with it a complete disruption to the existing normal operating procedures in most of the industries. The unprecedented situation due to the pandemic has struck some of the business functions disproportionately hard. The most impacted functions in the companies however are those where the workforces relied heavily on “on the field” presence for the execution of their work compared to those functions which could easily be converted into a remote working setup.

From the Life Sciences industry standpoint, the drug promotion via Medical Reps (MR) falls into the prior category. Although the industry as a whole has seen rapid adoption of digital solutions across the workstreams in the ongoing decade, their marketing efforts to the Health Care Providers (HCPs) still heavily rely on the Face to Face (F2F) interaction of the Reps with the Physicians.

This status quo however has been challenged by the ongoing COVID pandemic, with the social-distancing norms in place. There are estimates of 92% drop in F2F HCP engagements in April 2020 compared to 6 months ago[1]. It is also estimated that in the new post-pandemic normal, the frequency of F2F engagements will shift as much as by 65% to quarterly/annual rather than the weekly/monthly norms prevalent pre-COVID2. This is indeed a massive blow to the existing Pharma sales and marketing approach and has seen many of the companies rapidly scale up their digital engagement channels to fill the gap. The use of these digital channels for HCP engagement has seen a 2x increase from their pre-pandemic levels.[2]

The current COVID driven environment has several key implications for the Lifesciences organizations in their effort to meaningfully engage with HCPs.

Impact on Sales & Marketing Channel Mix – Restrictions on in-person meetings have lead to reduced access to HCPs, canceled/postponed training sessions, and canceled conferences and events, all of which were major marketing methods till now. Pharma and other Lifesciences companies have to accelerate their sluggish digital transformation initiatives and enable a true omnichannel digital experience for HCPs

Digital engagement channel optimization – The digital omnichannel push needs to account for varying pysician preferences for the type of digital channel engagement, based on factors like therapeutic area, demography, and personal preferences.

Personalized, contextual messages for better engagement– Physicians at the front lines have to balance innovation and efficiency while dealing with the increased pandemic workload. As a result, engagement and interaction frequency with HCPs have decreased abruptly. With this sudden shift, there is a need for communication to be crisp and contextual for it to be effective.

This brings us to an important question of how the Bio-Pharmaceutical companies should navigate the current shock concerning HCP engagement and what lies ahead for them. Pharma Commercial Teams would need a strategic HCP engagement approach that manages the immediate COVID situation as well as builds capabilities for the new digital-driven normal.

As the Bio-pharma companies scramble to optimize their marketing efforts in the current times, they need to formulate a strategy which tackles the problem in phases:

Now: Immediate Priorities to manage COVID situation (next 1-3 months) – Set of tactical initiatives and workarounds to the existing HCP engagement methodologies, meant to strictly tackle only the immediate priorities around COVID-19 impact

Next: Accelerate digital capabilities build-up to drive Omnichannel HCP engagement (in 3-6 months ) – Strategic initiatives to accelerate and deliver a highly engaging digital experience for HCPs. These will fundamentally help in shifting and realignment of biopharma omnichannel engagement capabilities in post-COVID realities.

(Now) Immediate Priorities to manage HCP promotions in COVID situation

As an immediate measure, Bio-Pharma companies need to evaluate the impact of COVID-19 on HCPs’ practice – Rx, patient counts, geographical impact, etc, and Field Reps access to HCPs. It is imperative that Biopharma companies create a COVID control room, which integrates external trigger impact data with internal data sources to truly assess the impact of COVID situation (and potentially other external triggers and shocks) on their sales & marketing plans.

As the COVID impact is quantified, bio-pharma can synthesize the same to adjust the tactical call plans for their promotional activities. The critical parameters to consider while making changes to the call action models would be:

Incorporate external COVID impact triggers at geo, HCP level

Defining and quantifying the digital affinity of physicians

Optimization of cross-channel (Digital & Rep) targeting frequency

Dynamic adjustments to the call-plan (digital mix, frequency) as the COVID situation evolves

(Next) Accelerate digital capabilities build-up to drive Omnichannel HCP engagement

Once the immediate priorities related to the pandemic are solved, companies can utilize the learnings and key insights from the pandemic times to further advance their digital engagement strategy. The evaluation of what went right and what were the misses in the earlier stage should also be used to formulate a long-term digital and omnichannel engagement strategy. There is also, a lot to learn from Digital-natives who have, highly effectively, leveraged digital channels to driven customer engagement.

Bringing these best-practices from Digital natives together with Bio-pharma context can help accelerate the digital transformation of the industries HCP engagement approach.

Best-practices and Learnings from Digital Natives

Lifesciences Ecosystem Context

Focus on differentiated HCP experience

Physicians have different interaction points, interests, and requirements including clinical content, CMEs, studies, samples, copay coupons, patient counseling material, etc. and hence differentiated experience enables engagement.

Volume and variety of data

Pharma has access to multi-dimensional physician data in terms of demography, preferences, prescription patterns, patient/payer mix profiles via claims, digital affinity to micro-segment physicians, and uncover preferences, behaviors, and personalized needs.

HCP/Customer Journey management and personalization

Advanced analytics and ML-based approaches can leverage the available data to predict intents, recommend interventions, and seamlessly deliver them via physician engagement platform and processes.

Omnichannel execution

Multi-channel interaction provides a foundation platform for delivering these experiences across digital as well as non-digital channels.

Measure, Learn & Improve

A/B testing driven digital engagement experimentation anchored on performance-driven, yet responsive targeting strategies.

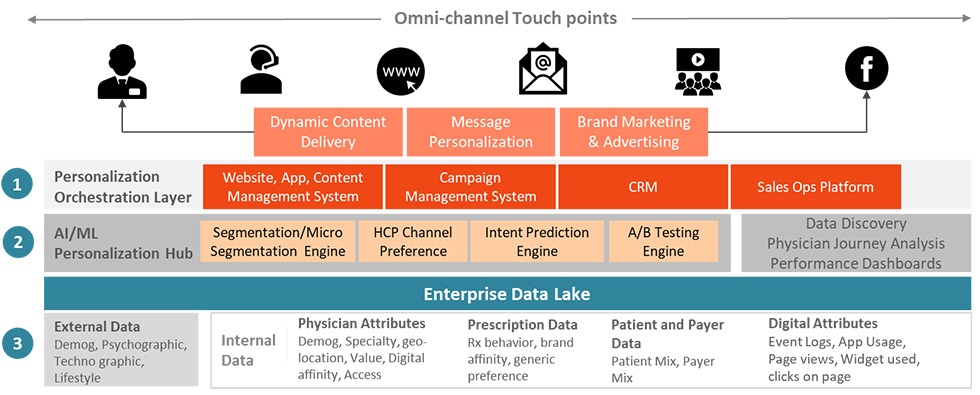

To accelerate their digital transformation journey, biopharma companies need to inculcate these best practices into their HCP digital marketing capability. An integrated Digital Engagement solution will help biopharma companies create and deliver omnichannel personalized experiences for HCPs, by enabling real-time AI/ML-driven next-best-action recommendations and precision targeting strategies based on their preference and intents.

COVID pandemic is an unprecedented global event, which will radically alter our behaviors, expectations, and interactions. Earlier rules of engagement are now getting irrelevant at a pace that is faster than ever before. To maintain(and grow) their share of voice and engagement with HCPs, bio-pharma organizations can no longer afford to follow the “digital-addon” approach. They have to fundamentally re-design their HCP engagement framework, as a Digital-driven strategy, $to stay relevant, to stay ahead and keep growing.

While the reckless overextension of credit lines by lenders and banks was the root cause of the financial crisis of 2007-09 and it had the US primarily as its central point, this time the financial crisis has been caused by a virus with rapidly evolving geographical centers and covering almost the entire world. The banks though are in a catch 22 situation, they need to support the government’s lending and loan relief measures while also maintaining low credit loss rates and enough capital provisioning for their balance sheet. Effective risk management and credit policy decisioning was never as challenging for the banks as it is now in the post covid-19 world.

COVID-19 implications and challenges for banks and lending institutions

Sudden shift in risk profile of retail and commercial customers – The surge in unemployment, deteriorated cash flow for businesses, etc has led to a sudden shift in the credit profile of customers. The data that banks used to leverage before COVID might not provide an accurate picture of the consumer’s risk profile in the current times.

Narrow window of opportunity to re-define credit policies – Bank’s credit policies in terms of origination, existing customer management, collections, etc have been designed over years with a lot of rigor, market tests, design and application of credit risk models and scorecards, etc. The coronavirus has caught the bankers and Chief Risk Officers by surprise and there is a narrow window of opportunity to make changes in existing models and risk strategies. While a lot of banks had built a practice of stress testing for unfavorable macroeconomic scenarios, the pace and impact of coronavirus have been unprecedented. This requires immediate response from the banks to mitigate the expected risks.

Government relief programs like payment moratoriums – The introduction of payment holidays and moratorium programs are effective to take some burden off consumers but prevent the banks from understanding high risk customers as there is no measure of delinquency that banks can capture from existing data.

Four-point action plan and strategy to navigate through the COVID-19 crisis

Banks will need to go back to the drawing board, re-imagine their credit strategy and put in accelerated war room efforts to leverage data and create personalized risk decisioning policies. Based on Incedo’s experience of supporting some of the mid-tier banks in the US for post COVID risk management, we believe the following could help banks and lenders make a fast shift to enhanced credit policies and mitigate portfolio risk

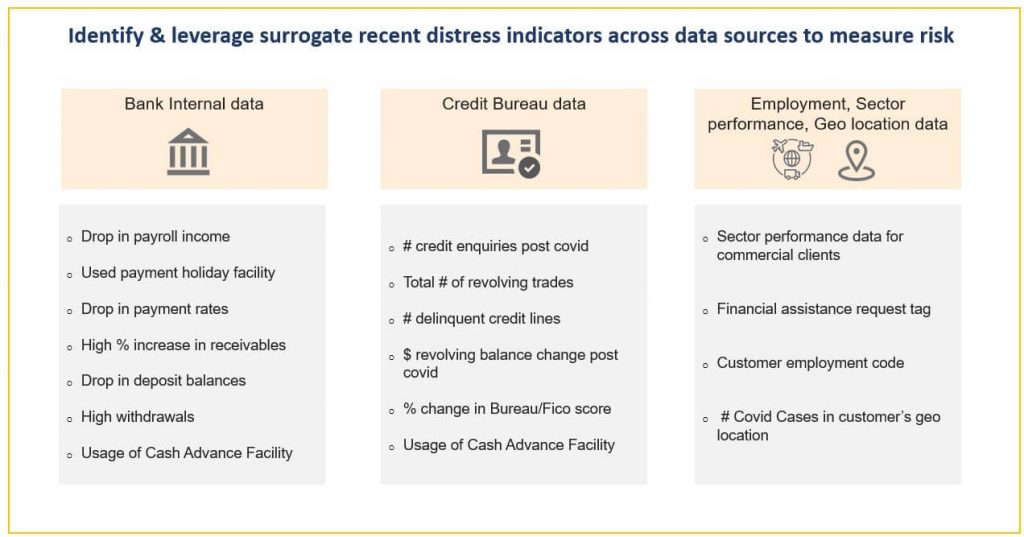

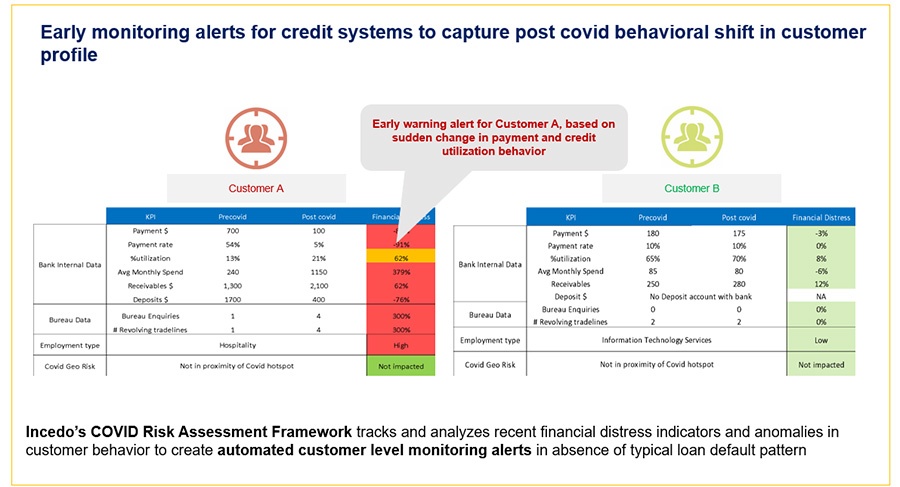

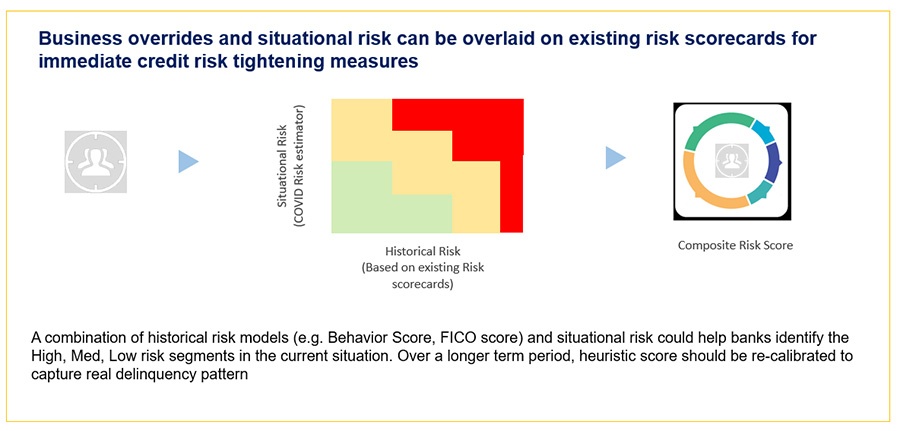

Covid situational risk assessment – As a starting point, Risk managers should identify the distress indicators that capture the situational risk posed post Covid-19. These indicators could be a firsthand source of customer’s situational risk (e.g. drop in payroll income) or surrogate variables like higher utilization or use of cash advance facility on credit card etc. Banks would need to leverage a combination of internal and external parameters, such as industry, geography, employment type, customer payment behavior, etc. to quantify COVID based situational risk for a given customer.

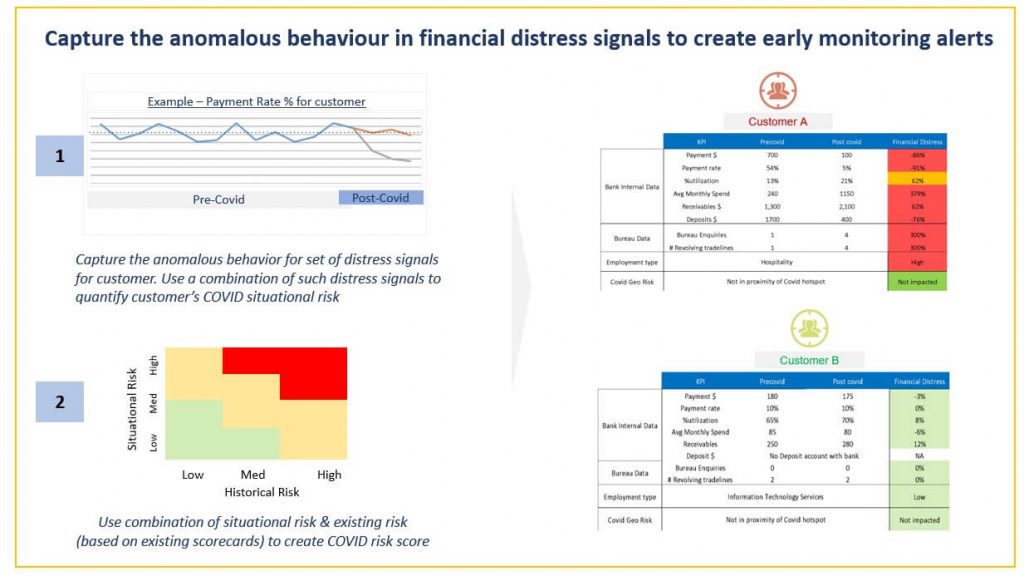

Early warning alerts & heuristic risk scores based on a recent behavioral shift in customer’s risk profile – A sudden change in the financial distress signals should be captured to create automated alerts at the customer level, this in combination with a historical risk of the customer (pre-COVID) should go as a key input variable into the overall risk decisioning process. The Early warning system should issue alerts, alerting the credit risk system of abnormal fluctuations and potential stress prone behavior for a given account.

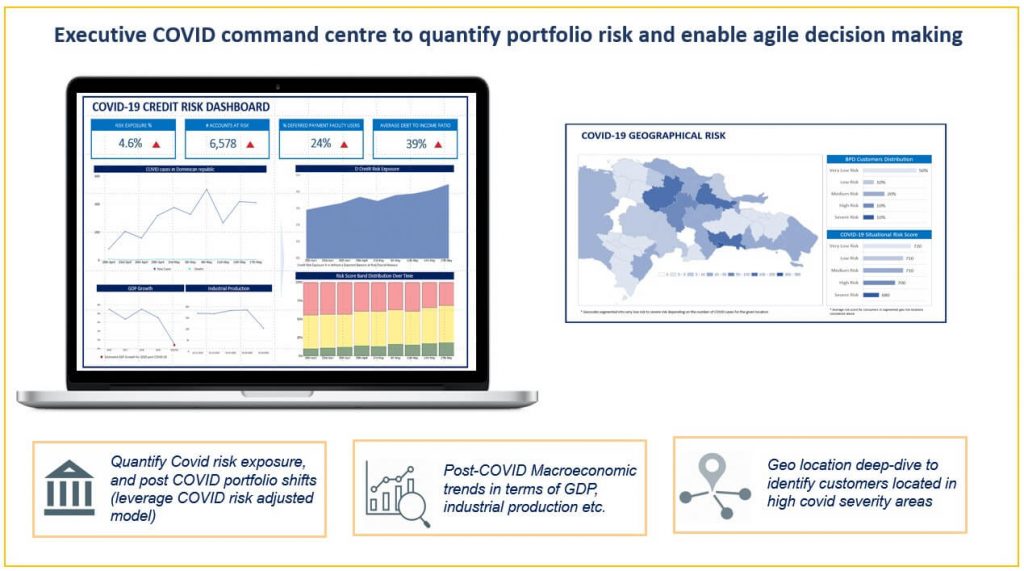

Executive Command Centre for COVID Risk Monitoring – The re-defined heuristic customer risk scores should be leveraged to quantify the overall risk exposure for the bank post COVID. Banks need to monitor the rapidly changing credit behavior of customers on a periodic basis and identify key opportunities. The rapid risk monitoring based command center should focus on risk across the customer lifecycle and various risk strategies and help provide answers to some of the following questions of the bank’s management team

What is overall current risk exposure and forecasted risk exposure over short term period?

How has the overall credit quality of existing customer base changed, are there any patterns across different credit product portfolios?

What type of customers are using payment moratoriums, what is the expected risk of default of such customer segments?

Quantification of the drop in income estimates at an overall portfolio level and how it could affect other credit interventions?

What models are witnessing significant deterioration in performance and may need re-calibration as high priority models?

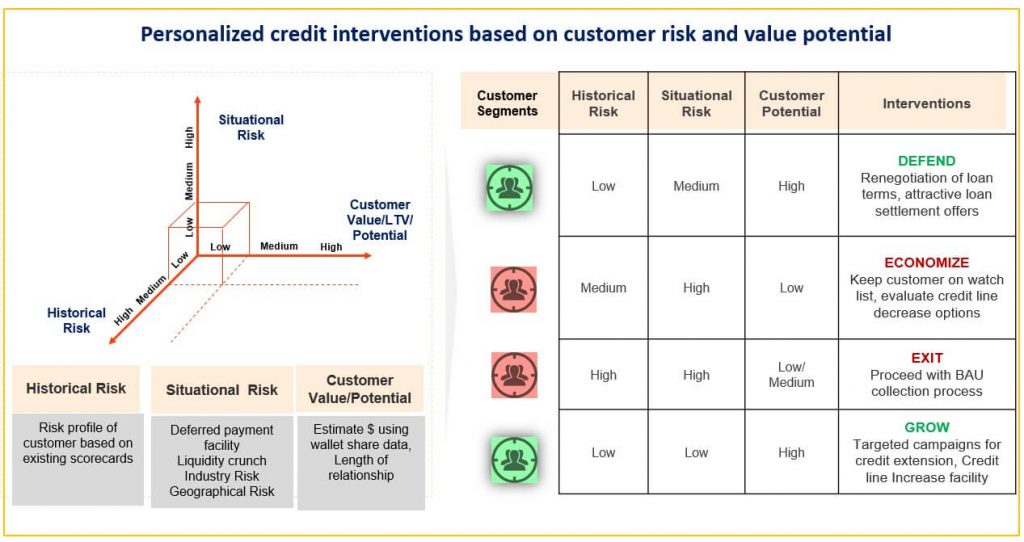

Personalized credit interventions strategy (Whom to Defend vs Grow vs Economize vs Exit) – To manage credit risk while optimizing the customer experience, banks should use data driven personalized interventions framework of Defend, Grow, Economize & Exit. Using customer’s historical risk, post COVID risk and potential future value-based framework, optimal credit intervention strategy should be carved out. This framework should enable banks to help customers with short term liquidity crunch through government relief programs, bank loan re-negotiation and settlement offers while building a better portfolio by sourcing credit to creditworthy customers in the current low interest rate environment.

The execution of the above-mentioned action plan should help banks to not only mitigate the expected surge in credit risk but also enable a competitive advantage as we move towards the new-normal. The rapid credit decisioning should be backed with more informed decision making and on an ongoing basis, the framework should be fine-tuned to reflect the real pattern of delinquencies.

Incedo with its team of credit risk experts and data scientists has enabled setting up the post COVID early monitoring system, heuristic post COVID risk scores and COVID command center for a couple of mid-tier US based banks over a period of last few weeks.

Learn more about how Incedo can help you with credit risk management.

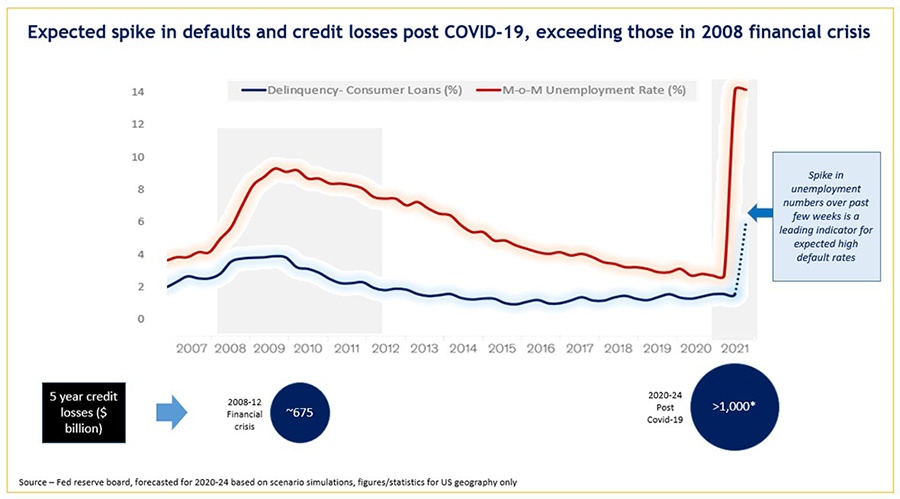

The magnitude of the spread of the COVID-19 pandemic has forced the world to come to a virtual halt, with a sharp negative impact on the economies worldwide. The last few weeks have seen one of the most brutal global equity collapse, spike in unemployment numbers, and negative GDP forecasts. With the crisis posing a major systemic financial risk, effective credit risk management in these times is the key imperative for the banks, fintech and lending institutions.

Expected spike in delinquencies and credit losses post COVID-19

The creditworthiness of banking customers for both retail and commercial portfolios has decreased drastically due to the sudden negative impact on their employment and income. In case of continuation of the epidemic for a longer-term period, the scenarios in terms of defaults and credit losses for banks could potentially be much higher than as observed in the global financial crisis of 2008.

Need for an up-to-date, agile and analytics driven credit decisioning framework:

The existing models that banks rely upon simply did not account for such a ‘black swan event’. The credit decisioning framework for banks based on existing risk models and business criteria would be suboptimal in assessing customer risk, putting the reliability of these models in doubt. There is an immediate need for banks to adapt new credit lending framework to quickly and effectively identify risks and make changes in their credit policies

Incedo’s risk management framework for the post COVID-19 world

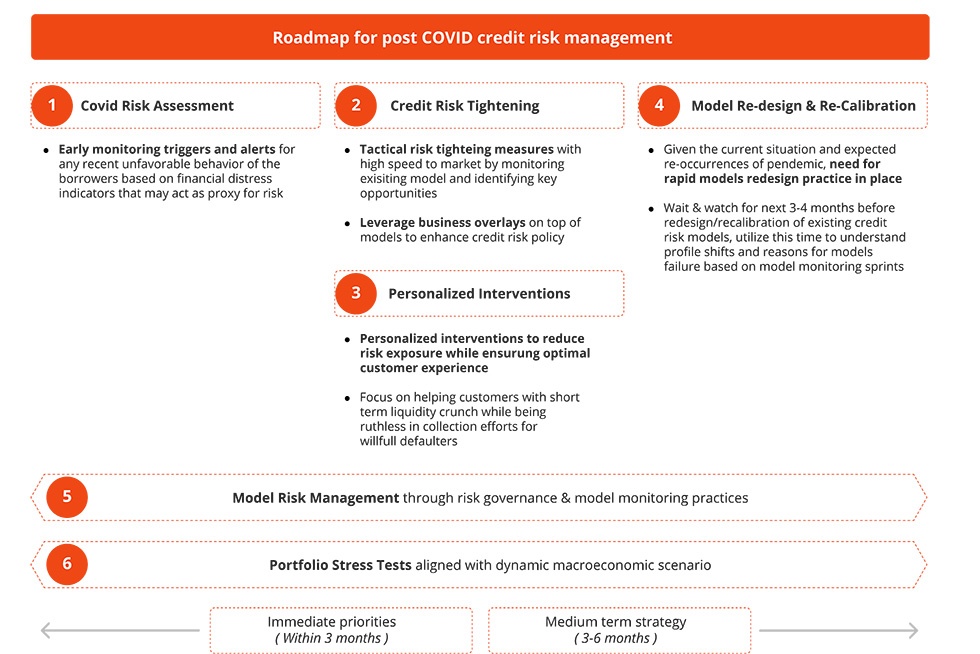

To address the challenges thrown up by the COVID-19, it is important to assess the short, medium and long-term impact on bank’s credit portfolio risk and define a clear roadmap as a strategic response focusing on changes to risk management methodologies, credit risk models and existing policies.

We propose a six-step framework for banks and lending institutions which comprises of the following approaches.

COVID Risk Assessment & Early monitoring Systems

Banks and lending institutions should focus on control room efforts and carry out a rapid re-assessment of customer and portfolio risk. This should be based on COVID situational risk distress indicators and anomalies observed in customer behaviour post COVID-19. As an example, sudden spike in utilization for a customer, less or no credit of salary in payroll account, usage of cash advance facility by transactor persona could potentially be examples of increasing situational risk for a given customer. In the absence of real delinquencies (due to moratorium or payment holidays facility), such triggers should enable banks to understand customer’s changing profiles and create automated alerts around the same.

Credit risk tightening measures

Whether you are a chief risk officer of a bank or a credit risk practitioner, by now you would have heard many times that all your previous credit risk models and scorecards would not hold and validate any longer. While that is true, it has also been observed that directionally most of these models would still rank order with only a few exceptions. These exceptions or business over-rides can be captured through early monitoring signals and overlaid on top of existing risk scores as a very short term plan. Customers with a low risk score and situational risk deterioration based on early monitoring triggers are the segments where credit policy needs to be tightened. As the delinquencies start getting captured, banks should re-create these models and identify the most optimal cutoffs for credit decisioning.

Personalized Credit Interventions

There are still customers with superior credit worthiness waiting to borrow for their financial needs. It is very important for banks to discern such customers from those that have a low ability to payback. To do this, banks require personalized interventions to reduce risk exposure while ensuring an optimal customer experience through data-driven personalized interventions. Banks need to help customers with liquidity crunch through Government relief programs, bank loan re-negotiation, and settlement offers while building a better portfolio by sourcing credit to ‘good’ customers in the current low rate environment.

Models Re-design and Re-Calibration

A wait and watch approach for the next 2-3 months period to understand the shifts in customer profile and behavior is a precursor before re-designing the existing models. This would enable banks to better understand the effect of the crisis on customer profiles and make intelligent scenarios around the future trend for delinquencies. There would be a need to re-calibrate or re-design the existing models. Periodic re-monitoring of new models would be a must, given the expected economic volatility for at least next 6-12 months period.

Model Risk Management through Risk Governance and Rapid Model Monitoring

There is an urgent need for banks to identify and quantify the risks emerging due to the use of historical credit risk models and scorecards through Model monitoring. While the risk associated with credit products has increased, the delinquencies have not yet started getting captured in the bank’s database due to the payment holiday period facility introduced by govt’s of most of the countries. In such a situation, it is critical to design risk governance rules for new models that may not have information related to dependent variables (e.g. delinquency) captured accurately.

Portfolio Stress Tests aligned with dynamic macro economic scenarios

Banks and lending institutions need to leverage and further build on their stress testing practice by running dynamic macro-economic scenarios on a periodic basis. The stress testing practice has enabled banks in the US to improve their capital provisioning and the COVID crisis should further enable banks across the geographies to use the stress tests to guide their future roadmap depending on how their financials would fare under different scenarios and take remedial actions.

The execution of the above-mentioned framework should ensure that banks and fintech’s are able to respond to immediate priorities to protect the downside while emerging stronger as we enter the new normal of the credit lending marketplace.

Incedo is at the forefront of helping organizations transform the risk management post COVID-19 through advanced analytics, while supporting broader efforts to maximize risk adjusted returns.

Our team of credit risk experts and data scientists has enabled setting up the post COVID early monitoring system, heuristic post COVID risk scores, and COVID command centre for a couple of mid-tier US based banks over a period of last few weeks.

Learn more about how Incedo can help with credit risk management.

Quantum Computing is the use of quantum-mechanical phenomena such as superposition and entanglement to perform computation. Quantum computers perform calculations based on the probability of an object’s state before it is measured – instead of just 1s or 0s – which means they have the potential to process more data compared to classical computers.

Why do companies need to reimagine their customer service? And why do they need to learn from Digital Natives like Google, Amazon, etc.? That is because these digital natives are setting the standard for customer expectations – In a recent survey, when customers were asked which company would they want to take Telecom services from, 60% people responded Google or Amazon!

So what are the key differences in the way Digital Natives approach Customer Service?

Fix at Source – While traditional organizations look to call deflection to save costs, digital natives believe that customer service indicates a customer pain point that should be fixed “at source”.

Use Product Thinking and Tech to solve issues – Too many processes and policies at legacy organizations are driven by risk, legal and finance making them high friction. Digital natives, start with the voice of the customer to design the right customer experiences and use technology to manage risks

Put AI and Technology at heart of everything – Not as siloed solutions to micro-problems but for driving end-to-end orchestration of customer experiences

To build next gen customer service capabilities, Incedo recommends 5 key initiatives:

Use Voice of Customer to drive business priorities

Fix root cause at source using Product Design Thinking

Personalise Service Channel Mix

Leverage AI to increase machine and self-serve digital channels

Use Cloud based architecture to enable AI driven Customer Service at scale

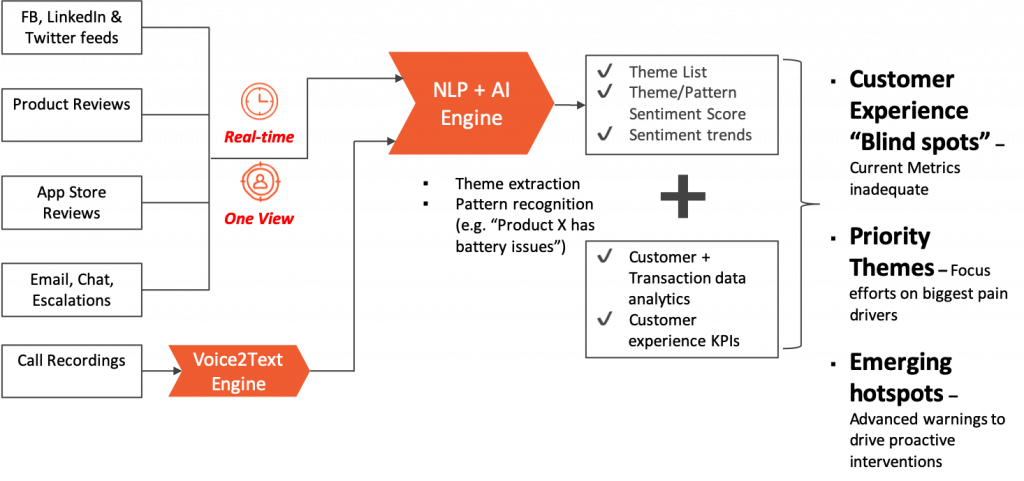

Voice of Customer to drive business priorities

KPIs to optimize: NPS

Customers talk about products and service through multiple medium – they leave reviews on product pages, social media, App Store, etc., call care, write emails or escalate to senior management. Often, the focus of customer service teams is on “managing” these inputs – douse the fire if the review is negative. However, there is a wealth of information available in these customer inputs on what is working and what is not – the challenge is that there is a lot of noise and traditional approaches have been inadequate. Advanced NLP + AI techniques can help organizations extract very actionable insights from these VOC channels

Fix root cause at source using Product Design Thinking

KPIs to optimize: Calls/Incidents per Unit/Order

Most customer service issues require cross-functional approach and product design thinking to resolve at the root cause. For example, when faced with fraud most organization end up putting strong checks and balances in place that also add a lot of friction to genuine customer journeys. Digital natives, on the other hand approach it differently:

They build robust tech and AI based preventive and corrective mechanisms and continuously refine them

They take a ROI based approach – compensating customers for small ticket breaches rather than adding friction

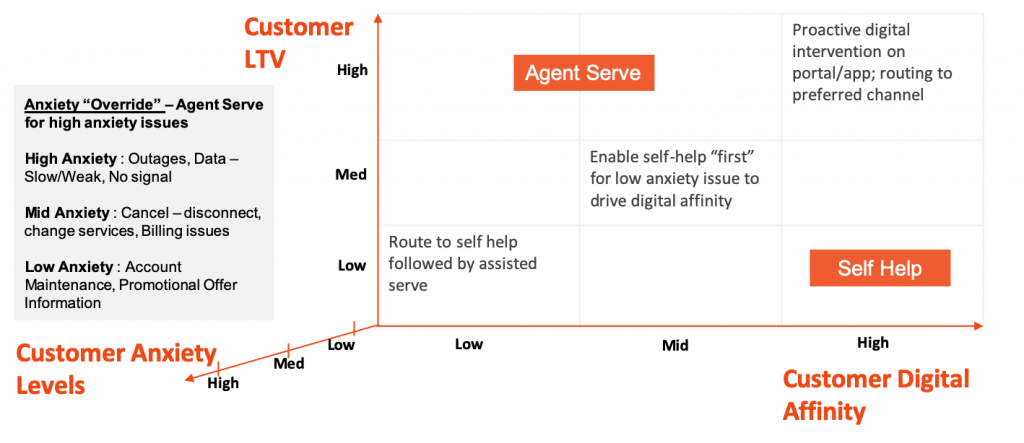

Personalize Service Channel Mix

KPIs to optimize: NPS, CSAT

A recent study showed that digital channel leads to highest customer satisfaction for service. However, all customers are not equal and so are the issues they face. Personalization of service channel based on following key parameters is recommended:

Customer lifetime value – High LTV customers expect white glove treatment best provided by high-quality agents

Digital affinity – Forcing low digital affinity customers towards digital channels and vice-versa can lead to dissatisfaction

Anxiety Levels – Some issues cause high anxiety, channels with best resolution rates if the customer is reaching out for these issues

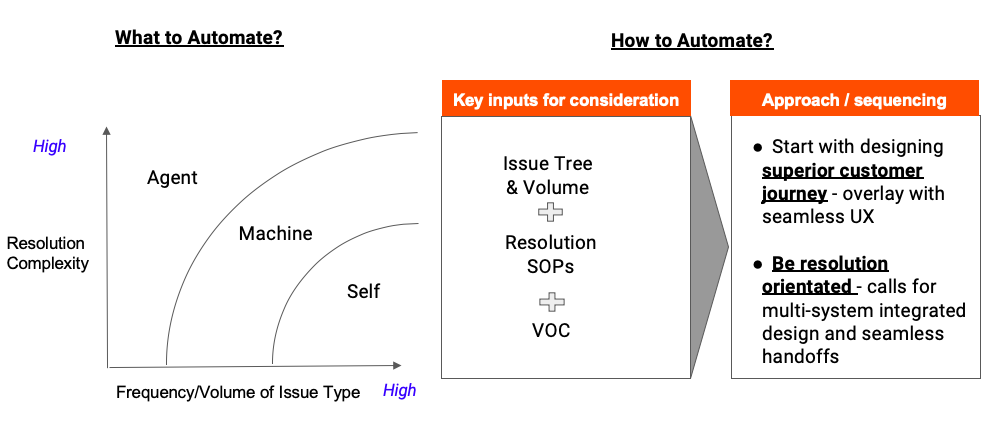

Leverage AI to increase machine and self-serve digital channels

KPIs to optimize: Resolution Rate, MTTR (Mean Time To Resolution), Operating Cost

What should you automate or move to self-service? The choice should be driven by volume and resolution complexity of issues. High volume, low complexity issues lend themselves well to self-serve channel whereas high complexity issues will require human touch. Design of chatbot and self-serve solutions should begin with design thinking of customer journeys

Use Cloud based architecture to enable AI driven Customer Service at scale

KPIs to optimize: Time to Market

The solutions and approaches outlined in the previous 4 initiatives require building real-time AI/ML models that evolve continuously. Traditional data and technology architectures cannot keep up with the velocity of change and volume of data. Cloud based architectures are key to solving this problem given inherent scalability and vast & growing libraries of reusable components.

However, transforming existing legacy architectures to cloud based is a daunting task. Organizations can follow a 2-speed approach to this transformation:

Speed 1: End to End Cloud transformation use case by use case

Speed 2: Building out the cloud architecture that can support multiple use cases and future needs

In conclusion, customer service as most organizations know it is transforming and Digital natives are at the forefront. Leaders of traditional organizations can drive this transformation by undertaking 5 key initiatives that put the customer at the heart of the service – to begin this journey a cross-functional empowered team that can own and drive these initiatives is recommended. It is either that or slow death as customers abandon sub-par experiences for better ones.

In a world of constant and extensive technology disruption, with organizations engaged in a battle for survival, the urgency to digitally transform is well understood by almost every large enterprise.