Enabling personalization at scale for consumer banks

Consider the case of a representative customer we’ll call Alex. Alex buys an iphone on his credit card and with this purchase, ends up utilizing around 90% of his credit limit. He gets a sms from his bank within minutes after his purchase, for a credit limit increase offer. With some more expenses expected in coming few days, Alex calls up the customer care and during discussions with call centre rep, is also given an option to convert his purchases into an EMI with attractive interest rate. Alex ends up opting for both Credit limit increase and EMI loan-on-card. What began as a single high-ticket item purchase, ended up becoming a much more engaging experience for Alex.

Welcome to the new world of data science enabled personalization. In the above case, Alex’s bank found that Alex (a credit worthy customer with good credit score) is in a need of extra credit and facilitated the next best action of offering credit limit increase through SMS channel. Not only that, bank’s data science algorithms also defined a price point for EMI loan-on-card to improve Alex’s chances of taking EMI loan and pushed that offer through call centre CRM. Such data-based personalized marketing strategy is the final goalpost for consumer banks to help enable strong customer experience, reduce churn and improve bottom line profitability.

While a very few digital natives and fintech players like Alex’s bank have been able to provide right one-to-one experience to their customer base, rest of the organizations still have a huge opportunity to leverage advanced data science practices and provide personalization on scale for their prospects and existing customers.

Based on our experience of working with some of the consumer banks in US and Latam markets, Incedo has developed a framework called Data Science Maturity Model for Consumer Banking Personalization. The framework describes the maturity levels that currently exist within data science teams for marketing personalization across the ecosystem.

In this post, we describe the Data Science Maturity Model and share the key challenges that are preventing banks from stepping up in their personalization journey to become hyper relevant to their customers.

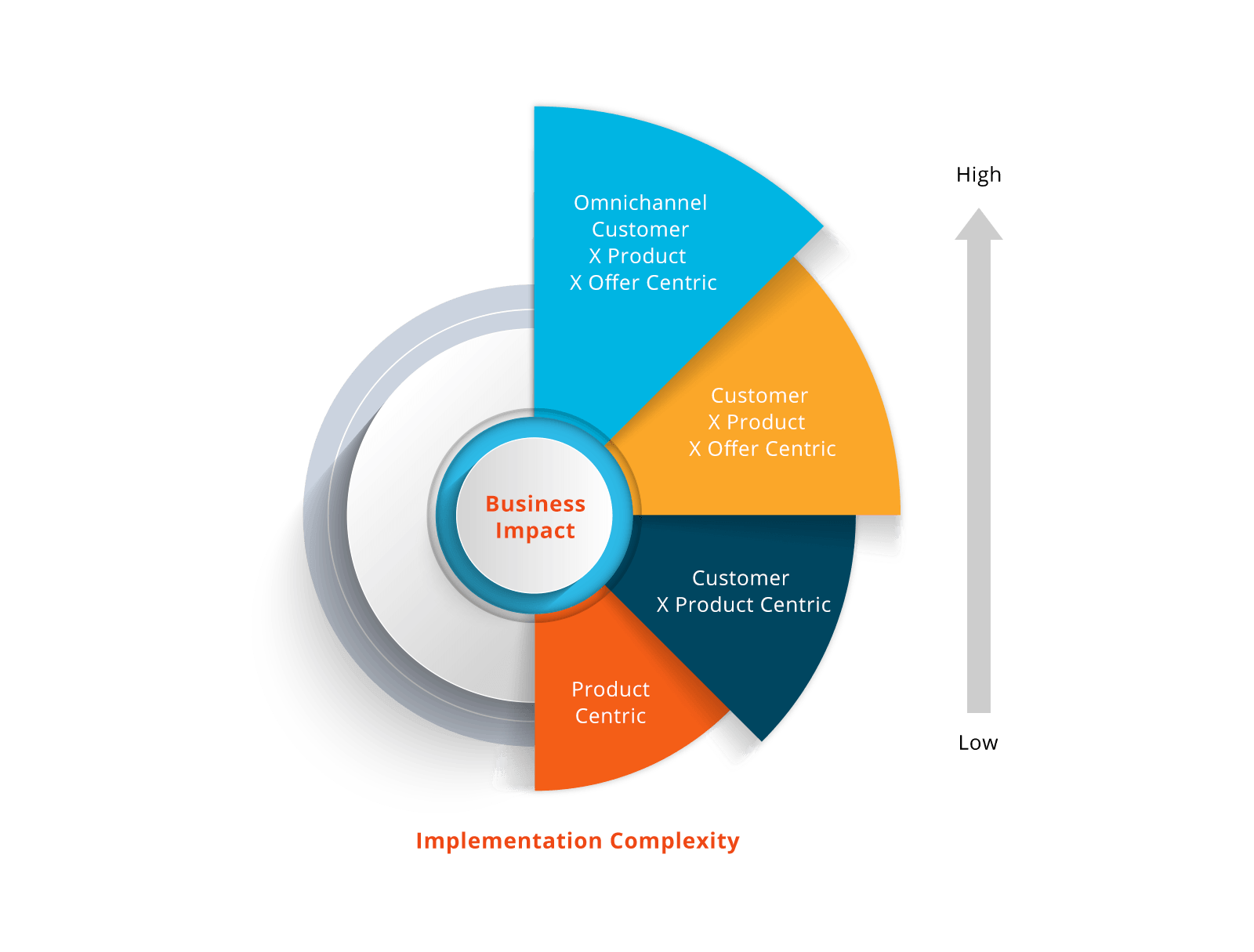

Stages of Maturity – Data Science Personalization Model for Consumer Banking

Based on our industry experience, it has been seen that banks tend to fall into four main stages of data science based banking personalization maturity

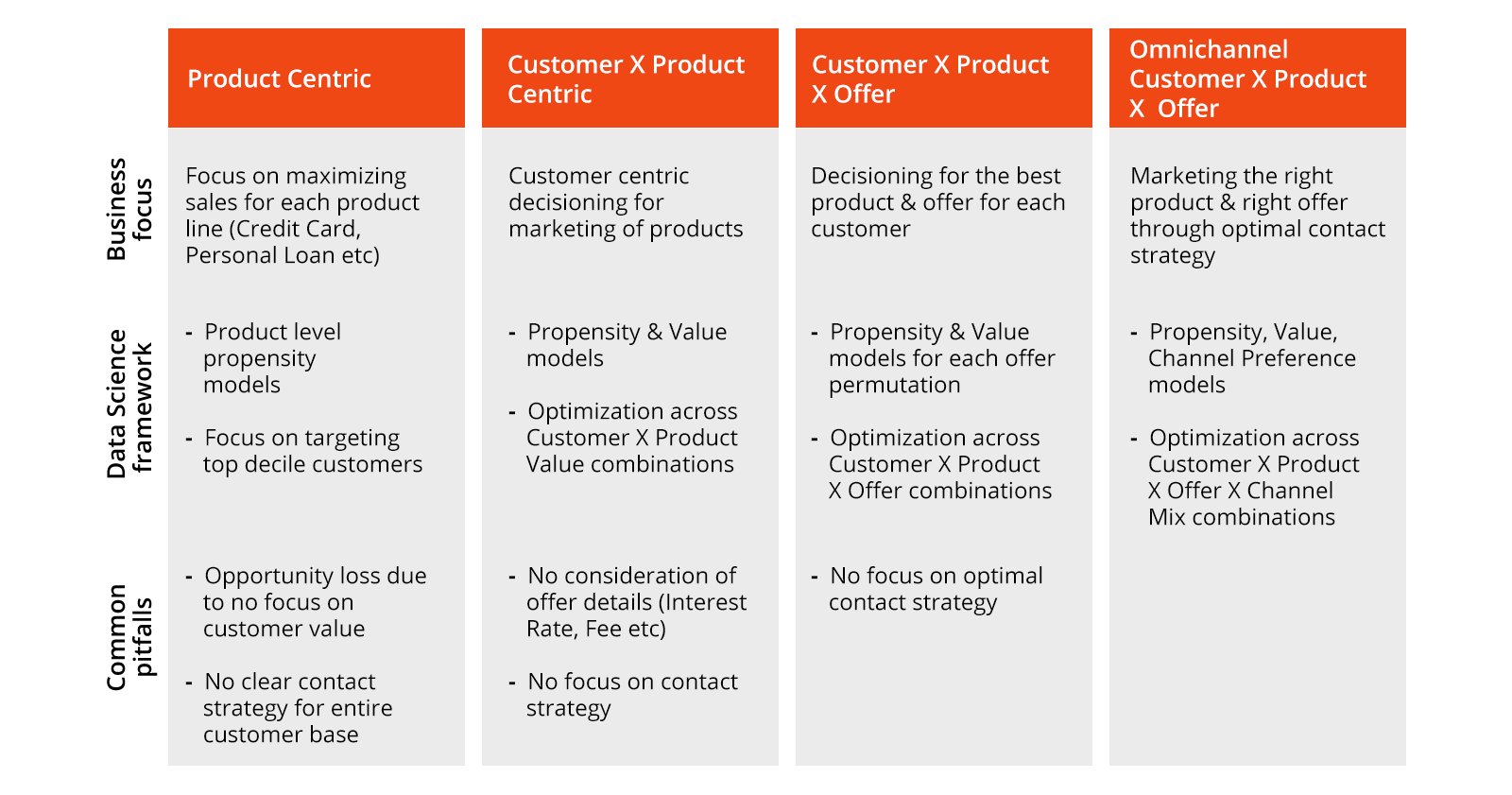

Level 1 : Product Centric

This is ground zero & is an approach used by most of the consumer banking institutions. The goal here is to look at analytics with a siloed product level focus. In context of a banking firm, products may include credit card, personal loan, mortgage etc.

The product heads typically focus on marketing-based strategies leveraging product propensity segmentation or models. The customers who fall in top deciles of each product model end up getting bombarded with offers while there are no contacts with prospects appearing in low deciles of these models. Since there is no focus on customer profitability or life time value, this approach is not optimal from both revenue maximization and customer experience point of view.

Level 2 : Customer X Product Centric

In this stage, firms look at customer management strategies to acquire, cross sell & upsell prospects. The focus is to look at product grid for each customer and identify which product would maximize firm’s profitability, while ensuring good chances of customer to take up the product. Consider an example where a customer has similar probability to take up both Product A and Product B and decision around next best product needs to be taken. In this case, the product which maximizes life time value for client is solicited to the customer.

Based on our experience of enabling customer centric product level recommendations for banks, the move from Level 1 to Level 2 of personalization can lead to incremental bottom-line impact of 10-15%, depending on the existing targeting framework being used at the organization.

Level 3: Customer X Product X Offer Centric

A personal loan offer with an APR of 12% vs APR of 18% would typically have different response propensities & profitability for the bank. For a price sensitive customer with good credit history, response rate would be much higher at 12% offer while bank’s margin & revenue would be higher for 18%. At this stage of personalization, decisioning models (response & value) are built for each Customer X Product X Offer permutation & business simulation & optimization exercises are carried out to identify optimal product & offer for each eligible customer. The final decisioning is based on what PnL KPIs business would want to maximize (e.g. # bookings, $ sales, $revenue etc)

In recent cases where we designed and implemented offer & pricing personalization strategy for our clients, there was an increase of ~10% in terms of revenue of the overall marketing program, in comparison to Level 2.

Level 4: Omnichannel Customer X Product X Offer strategy

The final stage of banking personalization journey involves focus on optimal contact strategy in terms of preferred channel of contact, frequency of contacts etc while also ensuring that right offer is selected for the customer. The data science engine would typically run the simulations based on different data science models to arrive at a personalized strategy for each customer in terms of product, offer & channel contacts, the optimal personalization is then enabled & fulfilled through front end operations teams (call centre, email etc). The right offer through right channel & creative helps improve customer experience & maximize bank’s profitability. While this stage helps maximize the incremental impact of data science initiatives for an organization, it comes with a trade-off in terms of high complexity of implementation.

What’s holding back the consumer banks from moving up the personalization analytics maturity curve?

If the incremental value gained through data science based personalization is so substantial and clear, why is it that not all the banks are already monetizing and achieving impact with it ?

The reason is that most of them continue to struggle with fundamental issues that prevent them from leveraging data science to drive the most optimal & personalized customer experience. These challenges span across data, technology and organizational areas and have been summarized below.

1. Lacking Data Quality & Technology Infrastructure

The first step and a must do in order to create value from data science is accessing all the information that is relevant to a given problem. This entails capturing and generation of data as a first step followed by integration of large stores of data from various sources.

While there are big data platforms and cloud-based services available to store massive amounts of data, the companies are still facing internal barriers in terms of data capture and quality of information. This in addition to long turnaround times to make a switch from legacy technology platforms is acting as a major bottleneck for organizations to build an accurate customer level data repository, which is a precursor to leveraging the state-of-the-art data science tools & algorithms.

2. Insufficient depth in Data Science Capabilities

Personalization is about treating each individual customer as a population of one and designing targeting strategies by leveraging features that encapsulate customer behavior in terms of product usage, spend habits, demographics, interactions across channels, customer journey at a point of time etc. Building such data science based solutions not only requires deep understanding of the sophisticated machine learning & deep learning algorithms but also involves clear understanding of the problem and running a series of business optimizations, before the final recommendations can be implemented in market.

In our experience, we found that most of the consumer banking organizations either don’t have sufficient depth in terms of data science talent and capabilities or have narrow focus on tools and techniques without clear roadmap on pragmatic implementation of data science solutions for driving business impact.

3. Siloed Organizational Structure

The operating model of data science organization for majority of banking institutions comprises of different data science teams operating as islands and tagged to each business unit.

As an example, during Incedo’s data science engagement with one of our client, we found that different data science teams were aligned to each of the product units (credit card, auto loan, personal loan etc) which prevented the firm from designing customer level omnichannel strategy across the product portfolio. The siloed operating model for data science prevents businesses from realizing best possible value from their analytics organization.

Personalized decisioning and targeting of products & offers is a critical imperative for consumer banking firms to operate in the competitive digital environment. To get there, organizations need to identify where they are currently in terms of data science maturity model and should create a roadmap to improve their personalization capabilities.

No matter what maturity stage you are in your data science based personalization journey, our team of experts can help you design and implement data science solutions that create bottom-line impact and provide seamless & wow experience for your prospects and customer base.

Over next few weeks, we would plan to explore and share our perspective in detail, on how to get around the three key challenges in personalization journey. Stay tuned!